Updated on: October 7, 2024 12:48 pm GMT

Understanding Broadcom’s Q3 Earnings and Its Impact on the Semiconductor Market

The semiconductor industry is undergoing a transformative shift, largely driven by the rising demand for artificial intelligence (AI) technologies. As tech giants race to capture market share in this lucrative sector, the focus often lands on key players like Broadcom (AVGO) and Marvell Technology (MRVL). With Broadcom set to release its Q3 earnings report soon, many investors find themselves asking: What does this mean for the broader chip market, and could there be potential investment opportunities? In this article, we’ll delve into the implications of Broadcom’s performance, the competitive landscape, and why Marvell Technology might offer a compelling alternative for investors.

Broadcom’s Dominance in the AI Chip Market

Founded in 1993, Broadcom has solidified itself as a heavyweight in the semiconductor world, particularly in the production of application-specific integrated circuits (ASICs). Its recent performance is a testament to its strong position in the market, especially as it pertains to AI chips.

Recent Growth Statistics

Over the past year, Broadcom’s stock has surged by an incredible 82%. Much of this growth can be attributed to its thriving AI chip segment. According to a report by JPMorgan, Broadcom is considered the second-most significant player in the AI chip market, following Nvidia. The company’s market share in ASICs is estimated to be between 55% and 60%, which has contributed significantly to its revenue growth and appeal to investors.

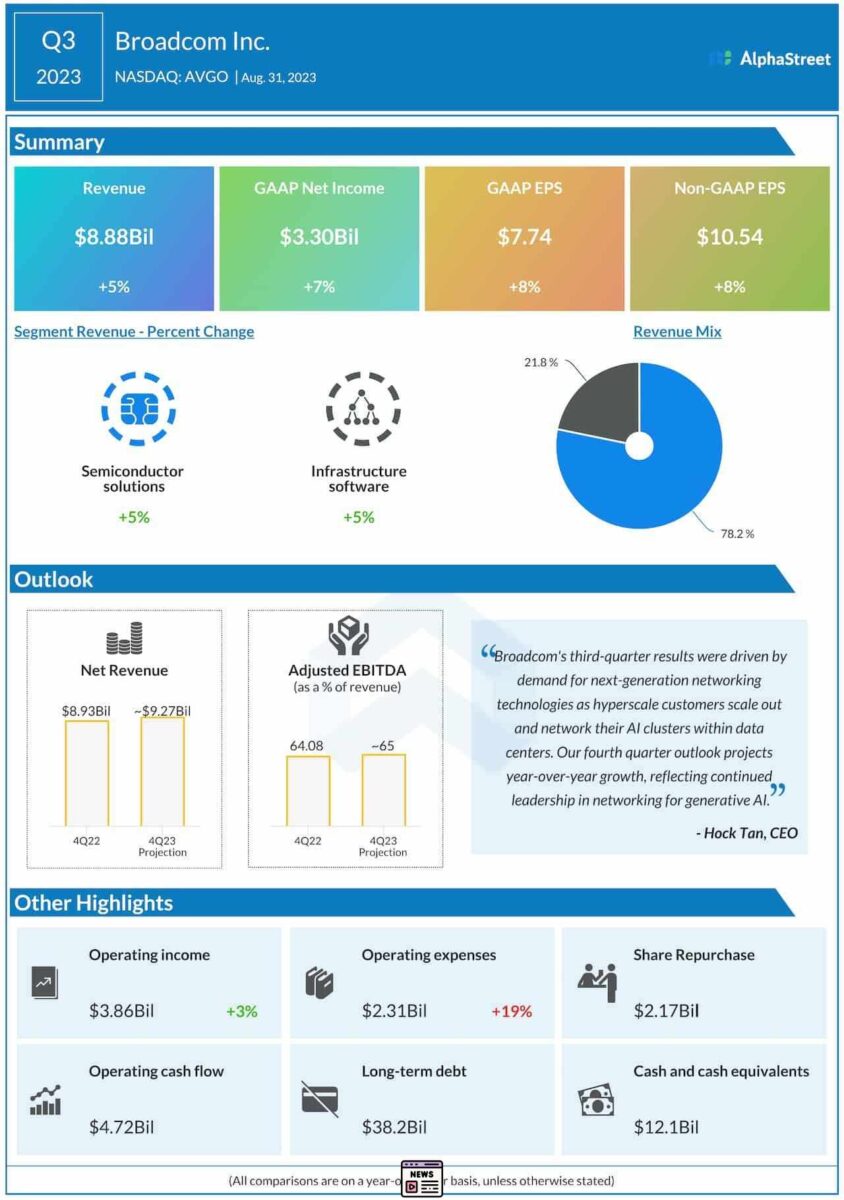

However, as shares have risen, concerns about an expensive valuation have surfaced. Currently, Broadcom trades at a price-to-sales ratio of 17 and a staggering 70 times its trailing earnings. For some investors, this might raise a red flag, prompting them to consider alternative investments.

Marvell Technology: An Attractive Alternative

For investors seeking exposure to the AI semiconductor sector without the hefty price tag associated with Broadcom, Marvell Technology presents a tantalizing option. Although Marvell’s financial report may initially appear underwhelming, a deeper analysis signals a promising outlook.

Performance Insights

Marvell reported a revenue decrease of 5% year-over-year for fiscal Q2 2025, finishing at $1.27 billion. During the same period, its non-GAAP earnings fell by 9%, amounting to $0.30 per share. Surprisingly, despite these declines, Marvell’s stock soared over 9% after the announcement, revealing investors’ confidence in its potential.

Why the Optimism?

The critical factor driving this optimism lies within Marvell’s data center segment, which generated a whopping $881 million in sales—a 92% increase from the previous year. This remarkable growth has positioned the data center business as a major revenue driver, comprising 69% of the company’s total revenue. CEO Matthew Murphy shared that their custom silicon programs for AI are advancing rapidly, with two chips entering volume production. This sets the stage for a significant rebound in revenues as AI chip demand escalates.

Future Revenue Expectations

Looking ahead, Marvell is on track to exceed its initial forecast of $1.5 billion in AI-related revenue for fiscal 2025. The company anticipates an acceleration in data center growth due to increased production of custom AI chips and a robust order book. Management has guided for a revenue of $1.45 billion for the current quarter, indicating a return to growth for the company.

Analysts have set favorable estimates for Marvell’s earnings trajectory, suggesting that the company could experience a resurgence in profitability, particularly as it approaches fiscal 2026.

The AI Chip Market: A Future Gold Rush

The market for custom AI chips is rapidly expanding, with JPMorgan forecasting a staggering cumulative revenue opportunity of $150 billion over the next four to five years. Broadcom, with its dominant market position, is expected to capture significant portions of this growth. Nonetheless, Marvell’s foothold—estimated at 15% of the ASIC market—positioning it as the second-largest player, allows it to benefit from this lucrative market as well.

Investment Potential in Marvell

Marvell’s current pricing structure presents a noteworthy opportunity for investors. Its price-to-sales ratio stands at a relatively modest 12.5, with a forward earnings multiple of 30, aligning closely with the Nasdaq-100 index. Should Marvell achieve an earnings per share of $3.41 in a couple of years and trade at 30 times earnings, the stock price could surge to approximately $102, suggesting a 34% upside from its current trading levels.

Market Trends Post-Broadcom’s Q3 Report

As Broadcom prepares to disclose its Q3 earnings, many analysts and investors are keenly examining broader market trends stemming from this report. A strong performance from Broadcom could help lift the semiconductor sector from its recent slump, primarily influenced by Nvidia’s stock fluctuations.

Potential Outcomes

1. **Positive Earnings Report**: If Broadcom exceeds expectations, it could spark renewed investor confidence, causing a ripple effect across chip stocks, including Marvell.

2. **Missed Expectations**: Conversely, if the results come in disappointing, it may heighten investor caution. This scenario could lead to price adjustments across the board, affecting not just Broadcom but also its competitors.

3. **Market Sentiment**: Regardless of the outcome, market sentiment surrounding AI technology continues to be bullish, suggesting continued investment interest in the semiconductor sector.

Conclusion: Investment Strategies Moving Forward

As we anticipate Broadcom’s Q3 earnings report, the semiconductor landscape remains dynamic and filled with opportunities for savvy investors. Broadcom’s immense position in the AI chip market underscores its growth potential, yet its high valuation may pave the way for alternatives like Marvell Technology.

Marvell offers a less expensive entry point into the lucrative AI chip arena, backed by strong operational growth and a promising future in data center expansions. Whether you lean towards Broadcom for its established prowess or choose Marvell for its growth potential, staying informed about market trends and earnings reports will be crucial in navigating this ever-evolving sector.

Doing careful research and looking into different investments in the semiconductor industry can help investors take advantage of the growing AI chip market. As competition gets tougher, it will be important for investors to match their strategies with how the market is doing to reach their financial goals in the future.